We are living in the age where the pace of innovation and disruption is getting faster and faster. As a result, keeping up with the latest-and-greatest technologies is becoming increasingly difficult, not to mention expensive. It seems that as soon as we upgrade our smartphone, a new model with a bigger screen and cooler features is released.

One word that comes with a lot of hype and confusion is “blockchain.” Because this technology is completely digital, thereby intangible, it’s tough to truly grasp exactly what it is.

Electric cooperatives know that with any new technology, we have to view it from every angle and consider how it will ultimately improve our services. With blockchain, that means recognizing its potential and limitations, both for Illinois’ electric co-ops and the energy industry as a whole. It also means asking whether blockchain truly benefits our consumer-members.

Let’s take a look at how blockchain works.

What is blockchain, exactly?

What is blockchain, exactly?

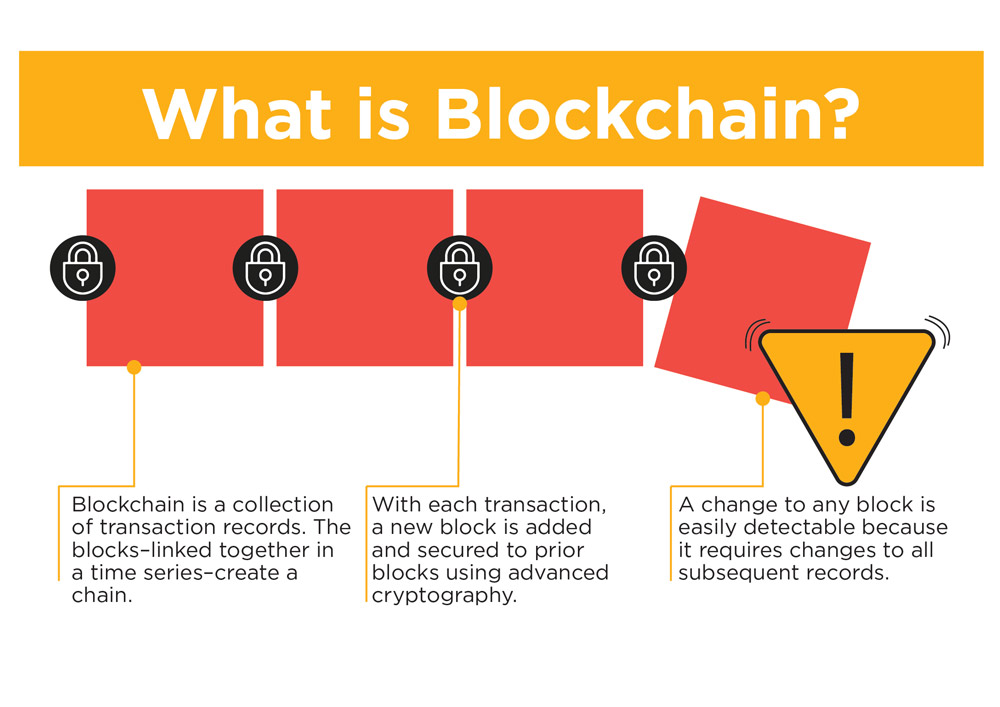

In simplest terms, blockchain is a digital, shared ledger that records transactions between buyers and sellers. The transaction records, or blocks, are linked together in a time series, or chain. When a new transaction is completed, a new block is added to the chain.

Electric co-ops make numerous transactions, such as billing, contracting with vendors and purchasing power on a daily basis, and even though we have secure, well-functioning systems already in place to handle these types of transactions, some see this as a potential application for blockchain and electric utilities.

What makes blockchain unique?

What makes blockchain technology so unique is that when a transaction takes place, it’s recorded on a network of computers, also known as nodes. The chain is shared and synchronized among all participating nodes in the blockchain network, making it very difficult to alter the chain without the interference being detected.

Another important characteristic of blockchain is that it’s decentralized. As noted before, a blockchain is distributed across the systems of all participating parties, rather than residing within a single institution, like a bank. This particular feature is why some consider the technology disruptive. Someone in Arkansas can send money to someone in Japan directly, without needing to go through a third party. This feature makes it transparent and eliminates the need for the trusted third party.

What are some real-life examples and applications of blockchain technology?

Currently, blockchain works best when the product being bought or sold is virtual rather than physical. If the transaction involves a material product, whether it be a new home thermostat or a jumbo jet, some trust agent is usually required to certify that the physical transfer actually takes place.

Eventually this technology may even start to intersect with areas of your life when recordkeeping and processing requires security, efficiency and connectivity. In the coming years, experts see potential for blockchain technology in the fields of healthcare, supply-chain management, finance and lending, and more. Blockchain could even change the way we prove our identity, as well as issue and maintain birth, wedding and death certificates.

Blockchain, like all software, is a means to an end that will provide different solutions to different needs, and determining its impact starts with understanding what the technology is and how it works.

Time will tell if blockchain proves useful for electric utilities in the future, but for now, we’re viewing this as a technology trend to watch. Our top priority will always be to provide our consumer-members with the safe, reliable and affordable energy they depend on.